Nerds Unite!Despite joking it's the only way I'd go to Miami, I'm excited to attend the first-ever Fintech NerdCon. Created by fintech nerds for fintech nerds, this is a place where "I'm in fintech" is a given and doesn't immediately end the conversation. Chase Changes Key Credit CardsNews broke just prior to publishing CardsFTW #160 last week of Chase’s upcoming changes to its flagship Chase Sapphire Reserve card. Since the brief mention in #160, I’ve had some time to dig into the changes.  Now, in business flavor First, a quick summary: - The Chase Sapphire Reserve consumer credit card’s annual fee is increasing to $795 per year, with a $195 fee for each authorized user.

- A new Chase Sapphire Reserve for Business card is available (also for $795) with no fee for employee cards

The $795 fee is eye-popping, but this isn’t the most expensive card. The Atlas Card is $1,000 annually; rumor has it American Express’s Centurion Card is $5,000 per year, following a $10,000 initiation fee. The new annual fee is also a large increase since Chase Sapphire Reserve’s introduction in 2016. The original fee was $450 ($602 in inflation-adjusted dollars), for a 32% increase. To make this fee increase more palatable, Chase is changing many of the rewards and benefits of the card. In addition, the coupon book approach to cards is alive and well. These “annual benefits just for being a cardholder” have been around for a long time (since at least 2010) and the updated CSR includes many of these: - $300 annual travel credit (still the most flexible travel credit available)

- $120 Global Entry, TSA Precheck or Nexus credit every four years

- $500 annual The Edit credit (Chase Travel’s collection of over 1,100 hand-picked hotels and resorts)

- A new $300 annual dining credit and primetime reservations at Sapphire Reserve Exclusive Tables, available for booking on OpenTable

- $250 annual value through complimentary subscriptions to Apple TV+ and Apple Music

- $300 annual StubHub credit on concert and event tickets

- $120 annual Lyft in-app credits, up to $10 monthly, plus 5x total points on eligible Lyft rides

- $300 annually in monthly DoorDash promos and complimentary DashPass membership worth $120 annually

- 10x points on eligible Peloton equipment and accessory purchases and up to $120 in annual statement credits toward Peloton memberships

Plus, there are even more benefits when you spend at least $75,000 per year (!): - IHG One Rewards Diamond Elite Status

- Southwest Airlines® A-List Status and a $500 Southwest Airlines credit when booked through Chase Travel

- $250 credit to The Shops at Chase

Chase says this set of benefits is worth $2,700 per year, so, by that measure, $795 is a deal, right? Well, it all depends on what you purchase. For example, I could see myself taking advantage of: - Annual travel credit

- Annual dining credit

- Lyft credits

- DoorDash credits

These credits add up to $1,020, so I am technically “coming out ahead.” Your mileage may vary. I know my friends at Kudos are working on trackers around this to help you understand if the fee is worth it. However, you don’t come to me for points-and-miles commentary, so let’s talk about the business of this all. When the CSR was launched, it was a big deal for a few key reasons: - Chase had poached a team from Amex to build a new product line to compete with the Amex Platinum, which at the time truly stood alone

- Chase spent more than $300 million launching the product, with an online and influencer focused campaign (we made something like $10MM at Bankrate from this launch) with a huge sign-up bonus (100,000 points)

- The CSR was the first card to specifically target a millennial demographic

At the time, millennials (the target demo) were much earlier in their careers and the discussion was "Will millennials use credit cards? Will millennials catch up?" I remember talking to many journalists about this topic. How many credit cards did you have nine years ago? Today, we know that the wealth of millennials has grown tremendously and the ongoing bifurcation of American income tiers (that is the hollowing out of the middle) means that there are increasingly more folks at the top end. For most Americans, a card of this level doesn’t make sense. Chase offers a Sapphire Preferred card with a much lower fee and the extremely popular Chase Freedom Flex card with no annual fee. Much like American Express effectively price-segments its users across Platinum, Gold, and Green, Chase is approaching a similar strategy. There might even be too many people with CSRs: if the lounges are always full and you can’t get access to the dining reservations then you will be dissatisfied. On the other hand, if you are a high-earning consumer in the prime of your adult life, then a card like this can make a lot of economic sense (not to mention the prestige factor, which is a part of the story). I think Chase is very smart and that this card will both continue to do well and be profitable for the bank. Adding a business version is savvy and enables Chase to continue to grab market share with entrepreneurs (for whom that business card $795 will be tax deductible). (Please consult your financial advisers on this one.) What’s next? Well, Amex has already tipped its hand that changes are coming to Platinum. The race continues.  Will Amex add new artists to their interesting card designs? I hope so (I have the top one).

Do you love CardsFTW? Share or forward this post to a friend!

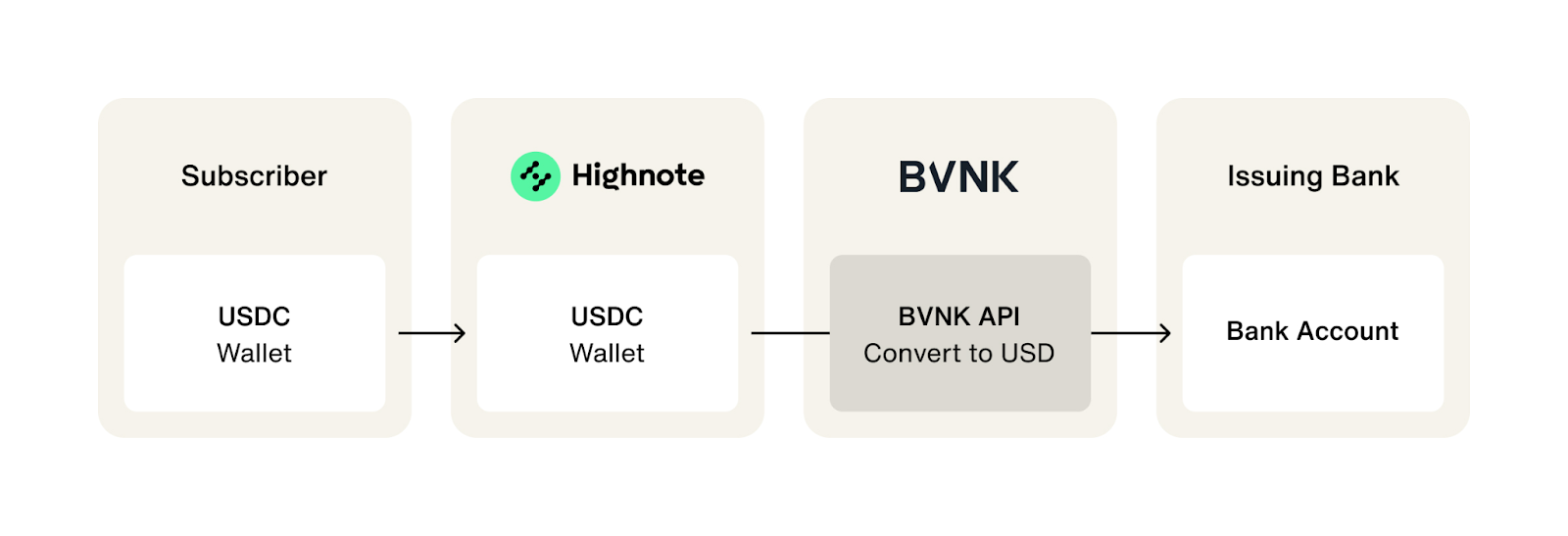

Stablecoin SettlementNothing is hotter in fintech than stablecoins. Well, maybe agentic payments. (I keep telling people to build an agentic stablecoin payment company and surf the hype wave.) Without getting bogged down in everything stablecoin, one piece of news caught my eye last week when Highnote announced a partnership with BVNK to launch stablecoin funding. Many people think of credit cards as real-time payments tools, but as we payment nerds like to point out: Visa and Mastercard are messaging networks; the actual money moves on other rails. When you swipe your Visa card at checkout, a message is sent to Visa and then to your bank to get an authorization. If that request is approved, and later a second message is sent to capture the funds, then Visa will instruct everyone to settle up. This happens via wire and ACH in the days following your transaction. For many modern card use cases there is a funding problem: if you run a corporate debit card program, for example, there must be funds sitting in a bank account prior to authorizing a transaction. If you were to use Highnote to run a debit card program, then you will need a settlement account at your partner bank with enough money in it at all times. Let’s say business grows rapidly; then you might needto have tens of millions of dollars in that account at any time. Given that funding that account via a wire or ACH can take time, and that funds don’t move via these networks on the weekends and holidays, this can really tie up your funds. Leaving $20 million at a bank for a few extra days is worth about $6,500 at 4% APY. Compounded over the course of the year and we’re talking about serious money ($~650,000 in this scenario). With stablecoin funding, you can submit a real-time payment request from your stablecoin wallet (which could be earning yield) that BVNK will transmit to your partner bank using a real-time payment push (FedNow or RTP), which allows you to keep your cards working and optimize your capital. This could be especially important when you have rapid growth periods or if you have to move money cross-border, where even a wire payment can take days (even domestic wires can take hours). The average cardholder doesn’t want (or need) to understand any of this, but as a payments nerd, I’m excited to see the real-world use cases for stablecoins starting to impact capabilities.

Thank you for subscribing to CardsFTW. Please consider supporting this newsletter by upgrading to a paid subscription today.

LendingClub CheckingSince the Dodd-Frank Act passed and limited interchange income on large bank debit cards, we have seen the disappearance of free checking and rewards at large banks. Last week, LendingClub, which also owns a bank, announced a new checking account product with no fees, competitive rates, and rewards.  That's a lot of cubes and boxes. The new account includes: - 1% cash back on gas, grocery, and pharmacy purchases

- 2% of LendingClub loan payments back (when paid on time)

- 1.00% APY on balances of $2,500

- No account fees or balance requirements

It’s very challenging to build a competitive debit card product given slim margins, but I love this approach and the tie-in to LendingClub loans. U.S. Bank + FiservU.S. Bank owns Elan Financial Services, which provides credit cards as an agent banking issuer for many smaller financial institutions. As more and more banks expand their credit card offerings, U.S. Bank announced a partnership with global payments giant Fiserv to integrate Elan into Fiserv’s credit platform. Fiserv’s Credit Choice platform is a fully managed credit card program designed to help smaller banks meet their customers’ financial needs, without exposing the bank to a lot of risk.  These are just some US Bank cards to make the newsletter have more images, but wow they have a lot of design stuff going on here. It’s quite interesting to see these two pair up, as I would have guessed from the outside that they are competitive with each other. As the credit card market continues to consolidate (see Capital One + Discover), smaller banks are going to need partners with increasing amounts of heft to compete. CardsFTWCardsFTW, released weekly on Wednesdays, offers insights and analysis on new credit and debit card industry products for consumers and providers. CardsFTW is authored and published by Matthew Goldman and the team at Totavi, a boutique consulting firm specializing in fintech product management & marketing. We bring real operational experience that varies from the earliest days of a startup to high-growth phases and public company leadership. Visit www.totavi.com to learn more. Interested in reaching our audience? You can sponsor CardsFTW.

|